How can we accelerate deep renovation and decarbonisation of building portfolios?

July 20th 2022

Decarbonisation in the building stock requires a significant acceleration of investments: More and better renovation projects have to be implemented, including investments in the building envelope to improve energy performance as well as investments in a decarbonised heating system. In particular, public and private building owners with large portfolios experience financial and staff-related resource limitations that have to be overcome in order to enable the acceleration of renovation and decarbonisation processes.

This was the topic of a workshop organised by the REFINE project in the frame of the eceee 2022 Summer Study on June 9th, 2022. In particular, the focus of the workshop was on practical implementation models which help owners of public and private non-residential building portfolios in overcoming financial limits. For example, a larger municipality may have insufficient budgets to implement a “renovation wave” for its schools, administration buildings, theatres, hospitals, etc. Similarly, a private owner may also have a lack of financial resources for the huge amount of decarbonisation investments required.

In this case, energy efficiency services (EES) combined with refinancing schemes are a promising way to speed up implementation patterns. Following this approach, EES providers address the reluctance or lacking capability of building owners to implement decarbonisation investments by incorporating financing into their service packages. Energy efficiency service (EES) is a widespread business model, where EE specialists (EES providers or ESCOs) offer integrated solutions from a single source (planning, implementation, operation, maintenance and monitoring) and take over a part of the investment risk through the provision of a performance guarantee. Furthermore, for many clients, it is attractive, if the EES provider is able to arrange the funding of the project (so-called Third-Party-Financing) so that the client can take advantage of the multiple benefits of investment into energy performance and decarbonisation without encumbering his own affordability and/or credit limits. In this case, the EES provider prefinances the investment and gets repaid through yearly remunerations which are dependent on the actual savings achieved. Therefore, the main source for repayment of any EES project financing is thus the cash flow generated by agreed and (many times) guaranteed energy cost savings. Refinancing then becomes important as it enables the EES providers to cope with these extensive investments by selling the receivables to be paid by the client to refinancing institution. In this way, the balance sheet of the EES provider is cleaned up, thus releasing financial leeway for new projects and business growth.

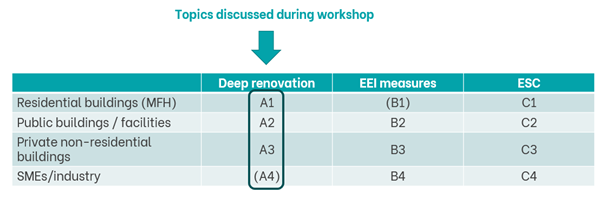

However, the discussions during the workshop made clear that there is no one-fits-all approach because of the different priorities of the clients. As the below table shows generally there exist different application fields for refinancing schemes in EES business, and it’s important that the best approach for a specific application field is selected.

Figure 1 Deep Renovation of Building Portfolios – Implementation Models for Acceleration

With respect to deep renovation in the non-residential building sector the market opportunities of combining EES with refinancing can be summarized as follows:

- Deep renovation of public building portfolios (A2): We observe that public building owners tend to implement deep renovation projects in a conventional way by “self-implementation”, one project after the other, as long as they can afford it. For larger portfolios, an EES approach combined with refinancing will lead to a pull-forward effect, i.e., the number of deep renovation and decarbonisation projects per year may increase beyond the given budgetary constraints. Although, when looking at a single project, this approach may be a bit more expensive, from a portfolio perspective the accelerated benefits from operational cost savings and sharply reduced energy price risks will prevail this disadvantage.

- Deep renovation of private non-residential building portfolios (A3): We assume that an EES targeting this application field is attractive mainly for owner-occupied buildings as well as for specific branches like hotel businesses that in many cases have limited access to financial resources.

The discussion during the workshop was substantiated by a case study from an Austrian public building portfolio manager who is preparing a 50 million investment programme with envisaged support of the ELENA Facility (European Local ENergy Assistance) which is sponsored by the European Investment Bank (EIB). As part of the preparation, a dynamic Life-Cycle Cost-Benefit Analyses (LCCBA) has been implemented, which shows that savings cash flows can refinance 60% to 70% of program cost, but not 100%! But we should look at this result the other way round! Based on the results of the LCCBA you only need 30%-40% of CAPEX for a deep building renovation and decarbonisation programme, harvesting immediately all the additional benefits, such as better resilience against energy price shocks, improved comfort, higher contribution to climate targets etc.

For the case of the public building owner this means that when applying the EES approach combined with refinancing with a public budget of only 15-20 million EUR an investment programme of 50 million could be managed – or the other way round, when compared with a conventional step-by-step approach, the implementation the whole investment programme could happen three times as quick!

Author: Klemens Leutgöb, e7 energy innovation & engineering