Sale of receivables from EPC projects in the Czech Republic is a successful example of refinancing EES

The goal of REFINE project is to contribute to the supply of sufficient and attractive financing sources to energy efficiency investments. The project is developing refinancing schemes enabling energy efficiency service (EES) providers to clean up their balance sheet, allowing for future investment in new projects.

Sale of receivables from EES projects in the Czech Republic provides a successful model example for the further development of the refinancing concepts suitable for other EU countries. In the Czech Republic, the receivables from most of the EPC projects in the public sector have been sold to one of the two commercial banks offering their services based on standardized contractual arrangements since 2007.

The scheme is mostly applied for public clients, most of which are municipalities and clients from the healthcare and education sectors. It is not used as often in the private sector, as the costs of sale of receivables are higher and banks need to conduct a more detailed financial analysis in advance.

An agreement on the future sale of receivables between the provider and the financial institution (FI) is usually signed before the procurement procedure begins. At the latest, it must be completed before final tenders are submitted and the winning EES provider is selected. All terms of the financing agreement are arranged exclusively between the EES provider and the FI. It also includes a fixed discount rate to be applied later to the purchase of receivables.

The approval of the sale of receivables is usually negotiated with the EES client in advance and incorporated in the EPC contract. However, in the Czech Republic, the sale of receivables is legally possible even if not mentioned in the EPC contract.

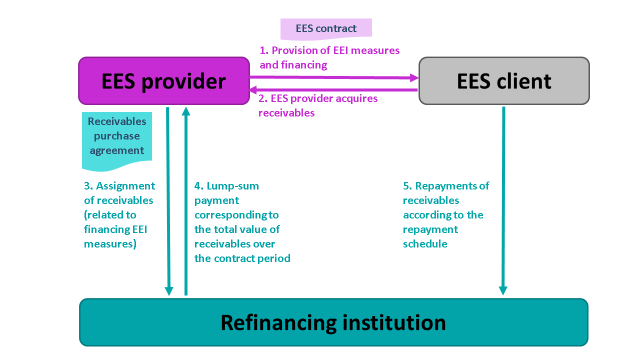

The steps of the sale of receivables to be seen on the picture below can be described in more detail as follows:

- The EES provider concludes the EPC contract with the EES client consisting of energy efficiency improvement (EEI) technology measures installations and a service component. The EEI technology measures are implemented according to the EPC contract. After the functionality of installed equipment is proved by testing, the EES client signs a handover report stating the work was handed over without defects.

- The EPC provider acquires receivables. The provider issues an invoice billing the client for the installation of equipment (consisting of costs of design, equipment, installation and financing). The EES client signs the invoice confirming its liability to repay the invoiced amount in stipulated repayments over the whole contract period. The client thus confirms the final price, usually accepting some deviations from the tendered price because of changes in the scope of EEI measures delivered.

- Receivables related to the financing of the EEI measures are assigned to the refinancing institution based on the receivables purchase agreement with the EES provider and the invoice with repayment schedule signed by the EES client.

- The refinancing institution sends a lump-sum payment to the EES provider corresponding to the total value of the receivables.

- The EES client sends regular repayments to the refinancing institution over the contract duration according to the repayment schedule previously confirmed by the client.

Figure 1 Process of sale of receivables the Czech Republic

After the EES provider sells the receivables from the EPC project to the financial institution (FI), it can invest the received payment into new projects. Another benefit is that the EPC provider eliminates the burden of the credit risk. This is crucial as the EES providers do not usually have expertise in credit risk evaluation. The sale of receivables is carried out without recourse on the EES provider, the liability being eliminated from the EPC provider’s accounting upon sale. On the other hand, the FI assumes only the credit risk of the client’s insolvency.

All other risks stay with the EES provider. After the receivables are sold, the EPC project is implemented according to the original EPC contract. Throughout the duration of the EPC contract, the EES provider assumes the contractually agreed performance risks of the project. These include the risks of not achieving contractually agreed savings as well as design risks, implementation risks and risks related to the operation of installed measures. If an EPC project fails to achieve the performance specified in the contract, the EPC provider is obligated by the contract with the client to compensate savings shortfalls that occurred over the life of the contract.

You can read more details on the sale of receivables scheme in the Czech Republic as well as on the other best practices from Austria, Belgium and Latvia in the REFINE Case Studies. The Czech case is also described in Czech language in the Czech news section of the REFINE website.